How regulators can stay ahead of evolving fraud tactics in an increasingly complex fintech ecosystem

AI changing the fraud landscape

Richy Emah, Regional Business Development Director at Sumsub, a global full-cycle verification and compliance platform, sits down with IT Edge News.Africa in an exclusive interview with Nana Theresa Timothy to examine the rapid growth and emerging challenges shaping Africa’s digital payment ecosystem.

Drawing from his extensive international experience in business development and compliance solutions, Richy Emah identifies AI-powered identity fraud as one of the most significant threats confronting the sector today. He points to the rising sophistication of deepfakes, synthetic identities, account takeovers, and digitally manipulated documents as key risks undermining trust in digital financial systems.

Emah argues that artificial intelligence represents a double-edged sword for the payments industry—fueling increasingly complex fraud schemes on one hand, while also emerging as one of the most powerful tools for fraud detection, identity verification, and scalable compliance on the other.

The interview offers critical insights into how African payment platforms, fintechs, and regulators can stay ahead of evolving fraud tactics while sustaining growth, inclusion, and confidence in the continent’s fast-expanding digital economy.

“Trust, Security, and Seamless Identity Verification becoming Increasingly Important”

Africa’s digital payment ecosystem is expanding rapidly. What are the biggest fraud and security threats currently facing the sector?

Africa’s digital payments ecosystem is growing at an unprecedented pace, driven by mobile money adoption, fintech innovation, e-commerce growth, and increasing cross-border transactions. However, this rapid expansion is also creating new opportunities for fraudsters.

RELATED: Why identity verification matters for mobile operators in Africa

One of the biggest threats currently facing the sector is AI-powered identity fraud, including deepfakes, synthetic identities, account takeovers, and digitally manipulated documents. Fraudsters are becoming more sophisticated and are increasingly using automation and generative AI tools to bypass traditional verification systems.

At the same time, financial institutions and fintechs across Africa are facing growing risks linked to mule accounts, phishing scams, social engineering attacks, and transaction fraud. Many legacy fraud prevention systems were not designed to deal with the speed, scale, and complexity of today’s digital financial environment.

RELATED: Digital identity verification spend will grow by 80% over next 5 years to $20b -Juniper Research

The challenge is particularly significant in fast-growing digital markets where financial inclusion is accelerating rapidly. As more users enter digital finance ecosystems for the first time, trust, security, and seamless identity verification become increasingly important.

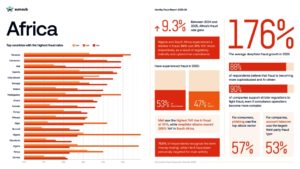

According to Sumsub’s Identity Fraud Report 2025–2026, some African markets are already seeing significant increases in AI-related fraud activity. South Africa, for example, recorded a 269% year-on-year increase in detected deepfake-related fraud activity, while Nigeria recorded the world’s highest share of synthetic document fraud cases in 2025 at 8%. Ghana also recorded a fraud rate of 4.6% in 2025, among the highest recorded across Africa.

“AI changing the fraud landscape”

How is AI, including deepfake technology, changing the fraud landscape for African financial institutions and fintechs?

Artificial intelligence is fundamentally reshaping the fraud landscape across Africa. Fraud is no longer only manual or opportunistic. It is becoming faster, more scalable, and increasingly difficult to detect using conventional systems.

Deepfake technology is one of the biggest emerging concerns. Fraudsters can now generate highly convincing fake videos, voice recordings, and identity documents designed to bypass onboarding and verification processes. These attacks are becoming more accessible and affordable through publicly available AI tools.

For African fintechs and financial institutions, this creates serious risks around identity verification, account security, onboarding fraud, and compliance. Criminals are also increasingly using AI to automate phishing campaigns, impersonate trusted individuals, and create synthetic identities using fragments of both real and fabricated information.

According to Sumsub’s Identity Fraud Report 2025–2026 and regional fraud analysis, South Africa recorded a 269% year-on-year increase in detected deepfake-related fraud activity, while nearly 10% of detected fraud cases in Kenya involved deepfake-related activity. Nigeria also recorded the world’s highest share of synthetic document fraud cases in 2025 at 8%, highlighting the growing sophistication of AI-enabled identity fraud across the continent.

What makes AI-enabled fraud especially dangerous is the speed at which it evolves. Traditional fraud detection systems often rely on static rules or periodic updates, while modern AI-driven attacks can adapt rapidly and become increasingly difficult to identify through legacy fraud controls alone.

This is why many organisations are shifting toward adaptive and AI-powered fraud prevention technologies capable of continuously learning and responding to new fraud patterns in real time. The industry is increasingly moving toward multilayered verification systems that combine biometric verification, liveness detection, behavioural analysis, transaction monitoring, and real-time risk assessment.

As digital finance adoption continues to grow across Africa, the ability to balance strong fraud prevention with seamless customer experiences will become one of the defining competitive advantages for fintechs and financial institutions.

“Compliance systems must reduce risk, support accessibility and inclusion”

As cross-border payments and financial inclusion grow across Africa, how can digital identity and compliance systems help build trust and security?

As digital payments and financial inclusion continue expanding across Africa, trust is becoming one of the most important foundations of sustainable growth. Financial institutions need reliable ways to verify users, prevent fraud, and maintain compliance without creating unnecessary friction for legitimate customers.

Digital identity systems play a critical role in reducing risks linked to impersonation, account fraud, identity theft, and illicit financial activity. Effective verification processes help ensure that users are genuinely who they claim to be while supporting safer digital onboarding experiences.

This becomes even more important as cross-border transactions continue increasing across West Africa and the wider continent. Fraud is increasingly borderless, while compliance systems and verification standards often remain fragmented across jurisdictions.

Technologies such as biometric verification, liveness detection, transaction monitoring, and ongoing risk screening are helping financial institutions strengthen trust while improving operational efficiency and security.

At the same time, compliance systems should not only focus on reducing risk. They also need to support accessibility and inclusion, particularly as millions of people across Africa continue entering the formal financial system through mobile-first digital platforms.

Long term, stronger collaboration between regulators, fintechs, financial institutions, and technology providers will be essential to building more secure and trusted digital finance ecosystems across Africa.

“Trust will become one of the most important competitive advantages for fintechs”

What practical steps should fintech startups, banks, and regulators take to strengthen fraud prevention while maintaining seamless customer experiences?

Fraud prevention and customer experience should no longer be treated as competing priorities. In today’s digital economy, users expect platforms to be both secure and frictionless.

Fintechs and banks should adopt layered, risk-based fraud prevention approaches that combine biometric verification, device intelligence, transaction monitoring, behavioural analysis, and real-time risk assessment. This allows organisations to apply stronger verification measures where necessary without creating friction for every user.

Financial institutions also need more adaptive fraud prevention systems capable of responding quickly to AI-driven attacks and evolving fraud tactics. Static verification systems are becoming less effective against increasingly sophisticated fraud methods.

Collaboration across the ecosystem is equally important. Fraud intelligence sharing between regulators, financial institutions, fintechs, and technology providers can help organisations identify emerging fraud patterns earlier and strengthen collective resilience.

Consumer education also remains critical. Many fraud schemes still rely heavily on impersonation, identity theft, and social engineering tactics targeting users directly.

At a regulatory level, balanced frameworks are needed to support innovation while maintaining strong security and compliance standards across digital financial ecosystems.

Ultimately, trust will become one of the most important competitive advantages for fintechs operating across Africa’s digital economy.

“Cross-border digital payments across Africa will continue growing as fintech ecosystems expand across the continent.”

Looking ahead, what major trends will shape the future of fraud prevention, payment security, and digital finance in Africa over the next five years?

Over the next five years, AI will likely become both one of the biggest drivers of fraud innovation and one of the most important tools for fraud prevention.

We expect fraud attacks to become more sophisticated, automated, and difficult to detect as deepfake technology, synthetic identity fraud, and AI-enabled impersonation continue evolving.

Digital identity verification is also expected to become more continuous and intelligence-driven. Instead of relying only on one-time onboarding checks, organisations will increasingly adopt ongoing monitoring, behavioural intelligence, biometric verification, and risk-based authentication models.

Cross-border digital payments across Africa are also likely to continue growing as financial inclusion, digital commerce, and fintech ecosystems expand across the continent. This will place greater importance on trusted digital identity systems, fraud prevention infrastructure, and stronger compliance capabilities.

We also expect organisations to place increasing focus on operational resilience, adaptive fraud detection, and real-time monitoring as fraud tactics become more complex and coordinated.

Ultimately, trust, security, and identity assurance will become even more important competitive differentiators for digital finance platforms operating across Africa.