A multi-trillion-dollar AI infrastructure cycle is now underway. But attention is moving beyond the headline AI developers. The real question is the physical constraints that will decide just how fast the industry can scale.

RELATED: SAS survey: Industry leaders on the quantum AI cusp

In this context, BestBrokers is sharing its latest report on the fastest-growing companies by AI revenue and the supply chain segments driving the next phase of AI expansion.

The AI build-out has translated into rapid revenue acceleration across semiconductor designers, memory producers, hyperscale cloud platforms, and emerging infrastructure providers.

Data shows who leads AI supply chain

To analyse these trends, the team at BestBrokers compiled and standardised AI-related revenue or the closest disclosed segment data from StockAnalysis across 20 publicly listed companies operating within the global AI supply chain.

The data shows how monetisation is distributed across the ecosystem and which segments have captured the strongest growth between 2021 and 2025. The data we collected can be accessed on Google Drive via this link.

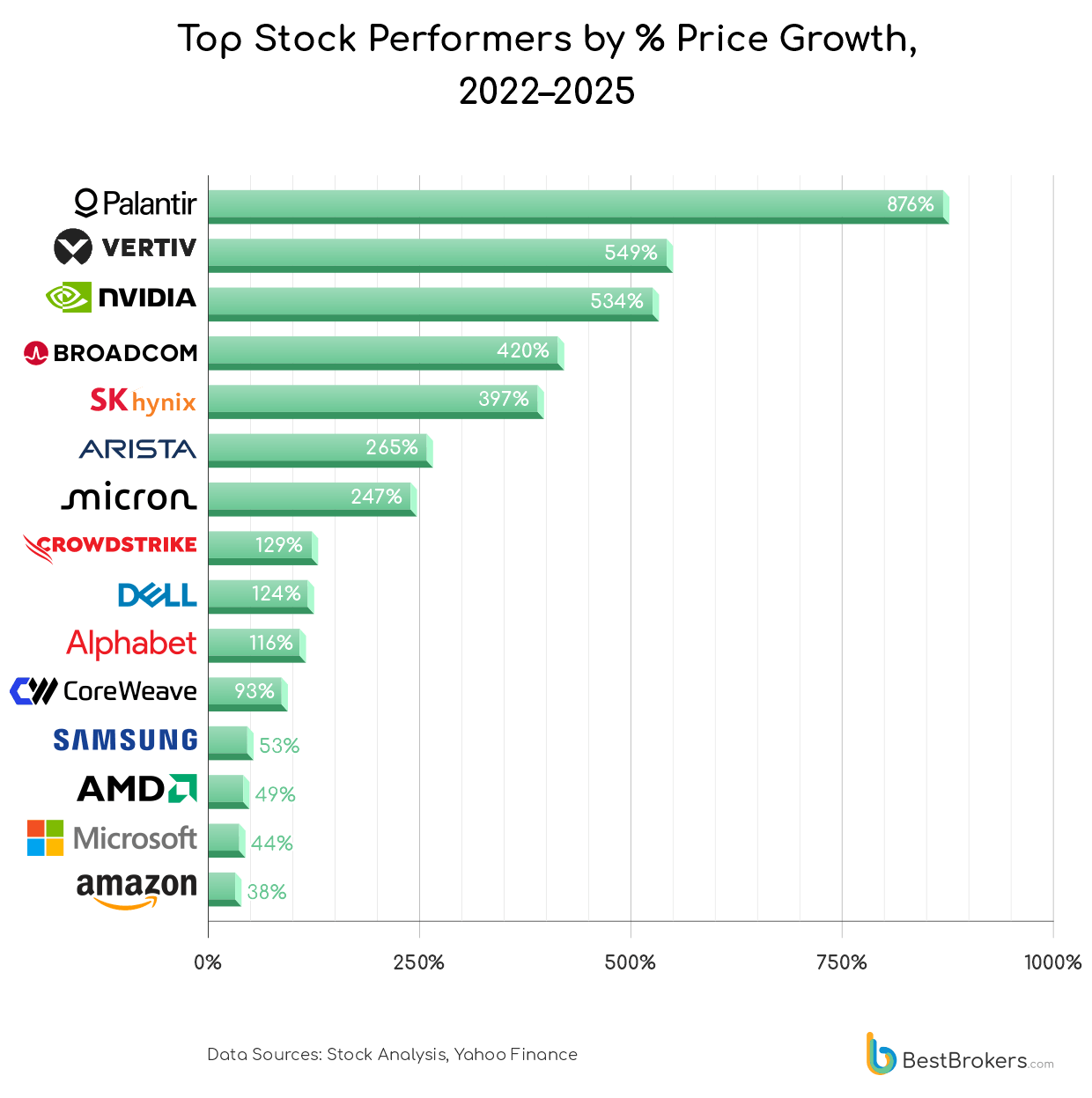

Data shows that two of the biggest winners of the AI boom were not chipmakers at all. Between 2021 and 2025, AI applications company Palantir Technologies and cooling systems provider Vertiv outpaced every major AI player in sheer market-cap growth. Palantir topped the dataset with a staggering 1,132% market value increase, rising from 36.5billionto449.8 billion. The surge came as investors re-assessed the company’s position in enterprise AI deployment and data-driven decision-making.

Vertiv Holdings, a key provider of cooling and power systems for AI-ready data centers, surged 583%. The company’s market capitalisation climbed from 9.4billionattheendof2021to64.1 billion by the end of 2025. The scale of that increase reflects the growing importance of the physical infrastructure required to support large-scale AI workloads.

AI Supply Chain Companies Ranked by Market Cap Growth (Year’s end 2021–2025)

- Palantir Technologies / AI Applications +1,132% (from $36.50B to $449.77B)

- Vertiv Holdings / Cooling & Infrastructure +583% (from $9.38B to $64.07B)

- NVIDIA / Compute +531% (from $735.27B to $4.638T)

- Broadcom / Compute +508% (from $274.73B to $1.67T)

- SK Hynix / Memory +279% (from $75.70B to $286.61B)

- Arista Networks / Networking +276% (from $44.17B to $166.02B)

- Micron Technology / Memory +207% (from $104.32B to $320.53B)

- CrowdStrike / AI Applications +158% (from $46.95B to $121.30B)

- Dell Technologies / Data Centers / Hyperscalers +102% (from $42.90B to $86.61B)

- AMD / Compute +101% (from $173.77B to $350.01B)

Other highlights from the report

- AI applications sit firmly at the top of the AI supply chain stack, with Palantir Technologies emerging as the most asymmetric winner in the dataset across both market-cap and equity performance. Its market cap surged 1,132% between 2021 and 2025 (from $36.5B to $449.8B), while its share price rose 876%, driven by the commercial scaling of its Artificial Intelligence Platform (AIP). This shifted Palantir from a data analytics vendor into an ‘operational AI layer’ embedded in enterprise and government decision systems, supporting accelerating adoption across defence, intelligence, and regulated industries.

- AI bottlenecks have proven to be a recipe for success, with Vertiv Holdings, a cooling company, emerging as one of the clearest beneficiaries of physical AI scaling constraints. Its market cap increased 583% between 2021 and 2025 (from $9.38B to $64.07B), while its share price rose 549%, reflecting investor re-pricing of thermal and power limitations in high-density data center environments. As AI workloads scale rapidly, Vertiv’s role in cooling, power distribution, and data center thermal management has become increasingly critical, positioning it as a key enabler of GPU-intensive infrastructure rather than a traditional industrial supplier.

- Firmly in the heart of the AI supply chain, NVIDIA has become the dominant AI chip supplier. Its market capitalisation expanded 531% between 2021 and 2025, rising to approximately $4.6 trillion, while its share price increased 534% over the same period. This performance was underpinned by an explosive expansion in AI-driven demand, with AI-related revenue growing from $14.6B in 2022 to $167.9B in 2025 (125% CAGR). The company’s GPU stack became the foundational infrastructure layer for training and inference workloads across hyperscalers, effectively positioning NVIDIA as the pricing and supply anchor of the AI compute market, with demand increasingly constrained by global data center build-out rather than chip design cycles.

Clear divergence between AI-specialised exposure and diversified semiconductor scale

- The memory layer shows a clear divergence between AI-specialised exposure and diversified semiconductor scale, with SK Hynix edging past Samsung Electronics across all key metrics. SK Hynix’s market capitalisation increased 279% between 2021 and 2025, alongside a 397% rise in share price, reflecting its strong positioning in high-bandwidth memory (HBM), a critical bottleneck component in large-scale AI training workloads and GPU clusters. In contrast, Samsung recorded a more modest 23% market-cap increase and 53% share-price gain over the same period, as its much larger and more diversified electronics and memory business diluted direct exposure to AI-specific demand growth.

- At the hyperscaler layer, Microsoft, Amazon, and Alphabet all delivered slower but consistent gains. Alphabet posted the highest growth, having its valuation rise from $1.92T in 2021 to $3.80T by the end of 2025. Compared to peers, Alphabet’s higher growth suggests greater perceived upside from AI-driven revenue transformation across both consumer and enterprise platforms. Amazon shows a similar infrastructure-led growth through its AWS cloud. Its market cap rose 47% (from $1.69T to $2.49T), while its stock increased 38.4% between 2021 and 2025. Microsoft sits at the center of enterprise AI infrastructure, delivering relatively steady but substantial scale-driven gains rather than bottleneck-style re-rating. Its market capitalisation increased 43.7% between 2021 and 2025 (from $2.52T to $3.63T), with its shares rising 43.8% over the same period.

Cost of removing physical bottlenecks across the AI stack

‘The data shows a clear shift in how value is being created in the AI ecosystem. While much of the attention remains focused on model development and compute acceleration, the most consistent outperformance is occurring in the infrastructure layers that enable those systems to scale. The market is effectively pricing in the cost of removing physical bottlenecks across the AI stack.’

– comments Paul Hoffman from BestBrokers.com.

Additional information on VC investments, major AI deals, and the full research methodology is available in the complete report. The dataset was compiled from StockAnalysis and company-reported financial disclosures, focusing on AI-relevant revenues, companies’ monetisation of the AI boom across the supply chain, and related stock performance trends for publicly listed firms operating within the global AI ecosystem.

The raw dataset is also available on Google Drive at the following link. Feel free to use the data or graphics, provided proper attribution is given with a link to the source.